Stocks and USD close higher heading into holiday period

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

Headlines

* Dollar strengthens after US labour, consumer sentiment data

* Traders show first sign of bailing on big Fed rate cut wagers

* OPEC+ struggle over African quotas forces delay to meeting

* Gold drops below $2000 as USD firms, yields recoup losses

FX: USD rebounded from a two-and-a-half month low for a second day off the 200-day SMA at 103.61. The weekly initial jobless claims data printed well below estimates.

EUR fell for a second straight day sliding to allow at 1.0852 before settling at 1.0888. Elevated inflation expectations plus the jobs data boosted the dollar and hurt the major. Focus turns to today’s PMI survey figures.

GBP dropped but rebounded off the 200-day SMA at 1.2450. The Budget revealed a series of tax cuts and other measures to boost growth. But a far more sluggish growth outlook than previously suspected was forecast. Tuesday had seen cable hit a 10-week high against the weaker dollar.

USD/JPY rebounded strongly back to the 50-day SMA at 149.53. This was mainly on the back of the rebounding dollar and yields modestly higher.

AUD consolidated its recent gains after running into resistance at the 200-day SMA at 0.6587. The midway point of the summer decline sits at 0.6584 to reinforce this zone.

Stocks: US equities closed higher with solid gains. The benchmark S&P 500 added 0.41% to settle at 4,556. The tech-heavy Nasdaq finished 0.43% higher at 16,001. The Dow settled 0.53% higher at 35,273. Economic data supported the idea that the economy remains resilient but also the Fed may be done with hiking rates. Stocks have tended to rise into Thanksgiving and into year end. Markets are closed for the holiday on Thursday. Nvidia fell 2.5% a day after the chip giant forecast Q4 revenue above estimates. But it warned US export curbs could lead to a sharp drop in Chinese sales.

Asian futures are in the green. APAC stocks trade mixed in Wednesday after the soft Wall Street handover. The ASX 200 was rangebound as tech and consumer sector losses were offset by defensive stock gains.

Gold dipped below $2000 to settle at $1989. The dollar bounced back while expectations the Fed will pause rate hikes limited the slide in bullion.

Day Ahead – PMIs to tick very modestly higher

PMI surveys are important leading indicators and point to the health of the economy going forward. Eurozone flash PMIs are expected to remain in contraction territory but move marginally higher. Manufacturing is forecast at 4.35 from 43.1 previously, services seen at 48.0 from 47.8 and the composite at 46.7, prior 46.5.

Other similar measures like the ZEW surveys have offered a glimmer of hope that the situation may be starting to improve. Commentary on inflation and the growth outlook within the survey period amid disinflationary themes will be digested. Better than expected numbers will perhaps boost sentiment that the worst is over in the eurozone. UK PMIs will also be released with weakness in services expected to keep the composite in check.

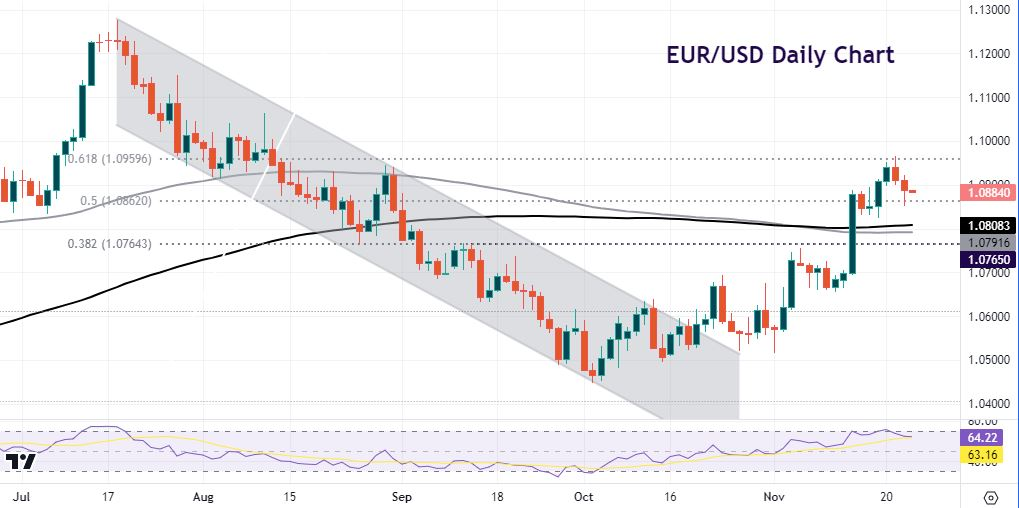

Chart of the Day – EUR/USD trying to consolidate

The world’s most popular currency major edged up to its highest since August on Tuesday. After falling below 1.05 in early October, the pair surged higher after the softer than expected US CPI data. Support should be seen around the 100- and 200-day SMAs at 1.0791-1.0808. The 50% level sits above here at 1.0862 for initial support. Prices topped out on the 61.8% Fib retrace level of the July decline at 1.0959. An upside PMI surprise could see EUR/USD take another look above 1.09.