Markets Lower on a Tightrope of AI and Persian Escalation

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

- Trump says Iran must ‘pay the price’ for delay on peace deal

- US inflation jumps to three-year high, but core metric cools

- Tech volatility continues as tech-heavy Nasdaq leads losers

- Gold tumbles more than 4% to fresh year-to-date lows below $4,100

Forex

USD was flat with mild strength on rising geopolitical tensions offset by the cooler than expected core US CPI data. Housing helped keep that metric soft – remember it is over 40% of the weighting in the CPI basket – and it is forecast to slide further in the coming months. The headline grabbed some headlines as it was the highest in three years, due to the 7% jump in gasoline prices. But that is likely to reverse in the June figures as gas prices eased. Fed rate hikes expectations got pared back with less than 25bps predicted by year-end. The Dolar Index printed an inside day and closed near its highs, which is not surprising considering all the current conflicting events.

EUR was steady buffeted by risk events in the form of the US inflation release and the upcoming ECB meeting. There’s around 68bp priced into the ECB for 2026 in total. See below for more details.

GBP touched the 200-day SMA at 1.3416 as the pound again outperformed most of its peers. The recent recovery in BoE rate expectations looks to have stalled, and yield spreads have steadied, offering little near-term directional risk for the pound. Eyes are on next week’s BoE meeting, as well as the June 18 by-election and possible future PM Burnham.

JPY softened marginally as the major continued edging higher. May PPI figures came in stronger than expected and a pace that is likely to maintain hawkish expectations into next week’s BoJ. A 25bps rate hike is baked in with one more move by December. The late April high sits at 160.72.

Stocks

US stocks: The S&P 500 lost 1.62% to close at 7,267, the Nasdaq closed down 1.98% at 28,508 and the Dow Jones settled lower by 1.87% at 49,924. Energy jumped 1.5% and Consumer Staples outperformed (+1.63%) while Industrials, Materials and Tech led the laggards. The VIX moved higher above 22 with both hardware and software tech names being sold. The latter has seen seven straight days of selling after prices had spiked back to flat on the year at the start of June, though semiconductors had been an even bigger driver of the tech sector’s drop last week. Micron, AMD and Broadcom all fell for a fourth time in five sessions. Oracle announced record Q4 and FY 2026 results driven by cloud infrastructure and cloud applications. But the stock moved down 5.8% after the close as it planned a debt and equity raise of $40bn in FY 2027. Super Micro Computer plunged 28% as it also planned to raise $7bn through equity offerings.

Asian Stocks: Futures are mixed. APAC mostly sold off on tech weakness again and US strikes on Iran. The ASX 200 did buck the trend with gains in financials and defensives. The Nikkei 225 slid as the tech-heavy index got hit. The Shanghai Composite and Hang Seng were lower on the escalating tensions in the Persian Gulf. Data was mixed with CPI printing softer-than-expected, but PPI topped forecasts and printed its highest since July 2022.

Gold

Gold fell to fresh lows again as it moved below the spike low at $4,098 seen in late March. Interestingly, oil prices haven’t been that strong in recent days even with all the conflicting headlines and threats between the US and Iran. Likely, a relatively hawkish Fed outlook and Middle East buyers turned sellers is seeing bugs get hit. Bullion is getting dumped as the latter use the proceeds for potential future reconstructions costs from the ongoing conflict.

Regarding oil, we note there have been reports of declining onshore crude inventories which suggest oil is leaving the Strait of Hormuz, despite not appearing in the official vessel traffic statistics. This is key for the growth and market outlook, with the physical delivery of oil being more important than the price itself.

Day Ahead – ECB Meeting

The ECB is expected to hike rates by 25bps to take the deposit Rate to 2.25%, given official communication seen during and after the last meeting in addition to multiple reports. Framing of the hike will be key given some officials have labelled the action as an “insurance” hike. Markets want to know if there is to be any subsequent tightening and at what point that could occur. That means the focus of the statement and especially President Lagarde’s press conference will be crucial around clues on what proportion of the Governing Council already expects to tighten again post-June.

The official line will likely remain data-dependent and stress optionality, particularly given the damage to the economy more generally from the energy shock. Updated quarterly staff projections should provide some insight, with inflation revised higher and growth cut. Ultimately, policymakers will need to strike a delicate balance between not calling the hike a ‘one-and-done’ hike while also stopping short of pre-announcing further hikes.

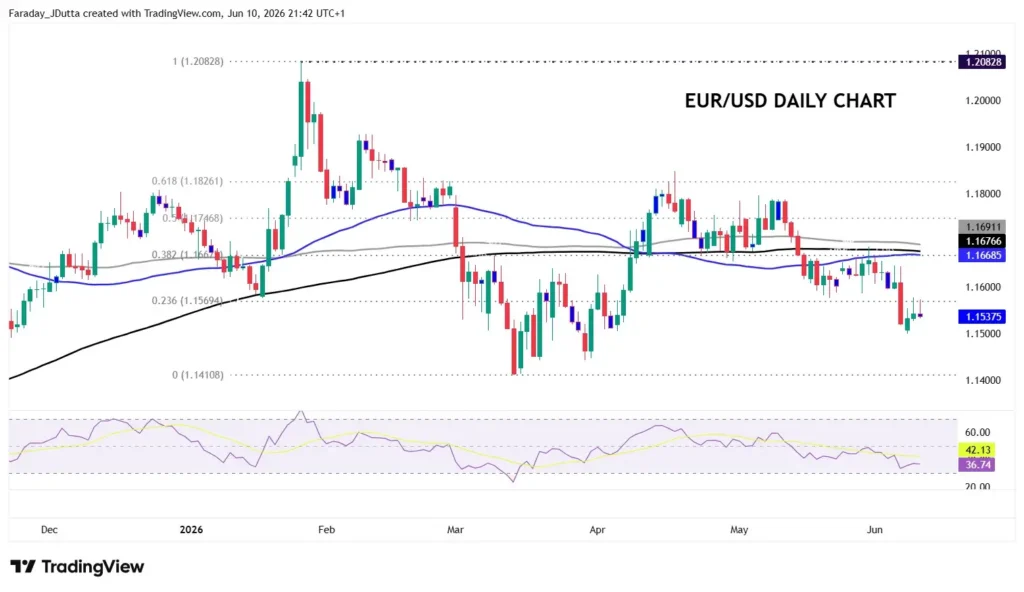

Chart of the Day – EUR/USD breakdown

We wrote last time about the world’s most popular currency pair being messy and tracking sideways below long-term SMAs. The breakdown after the strong NFP report on Friday has seen price consolidate between 1.15 and 1.1550. Bears will look to this week’s low at 1.1499 as an initial target before lows in late and mid-March. A more hawkish than expected ECB which fails to rule out back-to-back hikes could see the major find a small bid, with 1.1569 first short-term resistance. The 50-day SMA sits at 1.1668 and the 200-day SMA just above at 1.1676.